Executive Summary

On April 25, 2026, DeepSeek released V4 in two variants — V4 Pro (1.6 trillion total parameters, 49 billion active) and V4 Flash (284 billion total, 13 billion active) — both with a native 1 million-token context window. The headline benchmarks are respectable: V4 Pro Max-Thinking trades punches with Anthropic's Opus 4.7 and OpenAI's GPT-5.5 across most major evaluations, and edges ahead of Claude Opus 4.6 on LiveCodeBench (93.5 vs 88.8), Terminal-Bench (67.9 vs 65.4), and Codeforces (3,206 vs 3,168 for GPT-5.4). But the benchmarks are not the story.

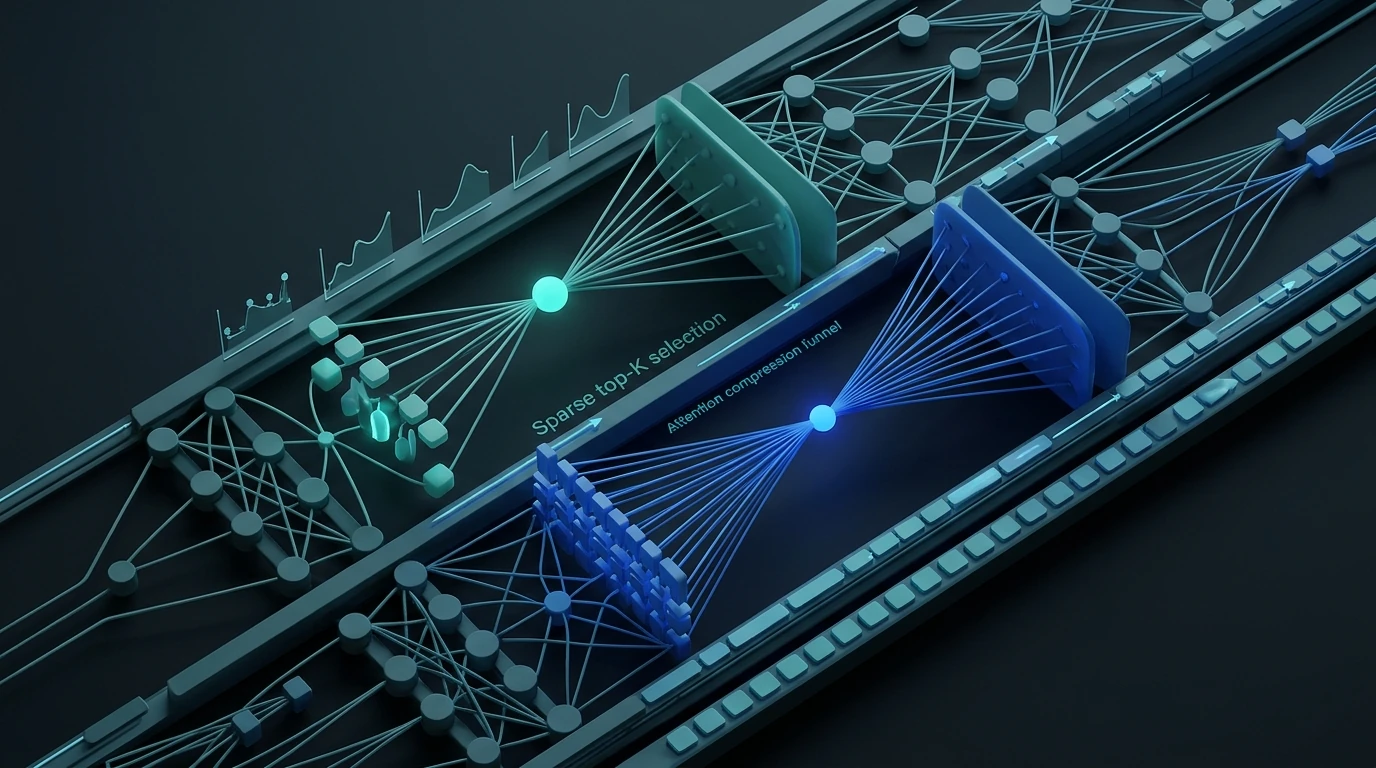

The story is the architecture. V4's hybrid Compressed Sparse Attention (CSA) and Heavy Compressed Attention (HCA) stack reduces the KV cache to 10% of V3.2's footprint at a 1 million-token context — a 90% reduction in memory overhead. On a GB300 NVL72 node, V3.2 required 35.60 GB of KV cache at 1 million tokens, limiting concurrent throughput to 4 sessions. V4 brings that figure to approximately 3.56 GB, enabling roughly 40 concurrent sessions on identical hardware. Since inference cost is memory-bound at scale, the throughput density improvement maps directly to a 10× reduction in per-request inference cost.

This is not a marginal efficiency gain. It is a structural repricing event for the enterprise AI market — arriving at the precise moment US frontier labs, pricing at $25–30 per million output tokens, are betting their capital structures on commanding a sustained premium for frontier capability.

Market Context

The AI model market in Q2 2026 operates on three assumptions: frontier models command premium pricing; frontier capability is the exclusive domain of well-capitalized US labs; and the gap between frontier and open-weight models is wide enough to justify the cost differential. DeepSeek V4 directly challenges all three.

The price differential is stark. DeepSeek V4 Pro is priced at $1.74 per million input tokens and $3.48 per million output tokens. V4 Flash runs at $0.14/$0.28. Anthropic's Opus 4.7 and OpenAI's GPT-5.5 sit at approximately $15–25 per million input and $25–30 per million output. At identical output volumes, an enterprise customer choosing V4 Pro over a comparable US frontier model sees a cost reduction of roughly 7–9×. That is not a price-performance optimization — it is a category shift.

Cache hit pricing extends the discount further. V4 Pro cache hits cost $0.14 per million tokens — a 12.4× internal discount versus fresh input at $1.74 per million. For agentic loops with stable system prompts — the dominant consumption pattern in enterprise deployments — the effective per-token cost collapses by an additional order of magnitude. A production agentic system running on V4 with a standard persistent context could see per-session costs one to two orders of magnitude below equivalent Anthropic API consumption.

The "near-frontier is good enough" argument, articulated by Matthew Berman in his April 25 analysis (YouTube), is not speculative. It follows from enterprise AI use-case distribution. The vast majority of enterprise workloads are not attempting to crack novel mathematical proofs or produce cutting-edge scientific research. They are automating document processing, customer interaction, code review, and internal knowledge retrieval — tasks where a model achieving 90–95% of frontier capability at one-eighth the cost represents a straightforwardly rational substitution.

Two independent data points from the same week sharpen the timing. Anthropic's "demand-rich, compute-starved" characterisation reached mainstream commentary, with quota manipulation described as a stealth price hike tool that raises headline subscriber prices without formal announcement (Lev Selector, April 25). OpenAI's GPT-5.5 launched simultaneously at $30/M output, deepening the US lab pricing cluster at the top end. DeepSeek V4's arrival into this environment is structurally disruptive rather than merely competitive — it compresses the premium at the moment US labs are most exposed to a cost-comparison argument.

Players

DeepSeek is unusual in the frontier model space for combining deep technical transparency with aggressive open-weight releases. The V4 white paper is more detailed than anything OpenAI or Anthropic have published for comparable flagship models, including candid acknowledgment of failures and compute constraints. The paper notes that Pro service capacity remains limited until "950 super nodes" — a reference to Huawei Ascend 950-based supercomputing infrastructure — are deployed at scale in H2 2026, after which prices are expected to drop significantly. This is simultaneously a candid admission of current operational limits and a forward price signal that progressively worsens the competitive position of US frontier labs.

Huawei entered the picture in a formally significant way on April 24, when Reuters confirmed that its Ascend supernode — based on the Ascend 950 AI chips — would fully support DeepSeek V4 at launch (Reuters). This is not a peripheral detail. US export controls restrict the sale of Nvidia's highest-tier chips — including the GB300 — to Chinese buyers. DeepSeek V4 was developed and deployed on hardware operating under those constraints. The Huawei Ascend 950 alignment represents an accelerating path to Chinese hardware independence: when the 950 supernode rollout completes in H2 2026, DeepSeek will operate a full-stack Chinese AI infrastructure — hardware, model, inference, and API — with no US component in the critical path.

Anthropic is named directly in the benchmark comparisons and in the distillation-attack reporting. The US government's formal acknowledgment of foreign distillation campaigns, via Director Michael Kratzios's April 25 statement, references US AI labs collectively, but Anthropic published the most quantified analysis: DeepSeek exchanged approximately 150,000 queries against Claude, compared to Moonshot's 3.4 million and Minimax's 13 million. Berman's analysis (YouTube) draws the correct inference: 150,000 exchanges are insufficient to explain V4's capability level — the algorithmic innovation is real, not a laundered IP transfer. Anthropic's dual problem — compute constraints and V4's pricing — is structurally uncomfortable.

OpenAI launched GPT-5.5 the same week at $30/M output, positioned as the most capable model for agentic and coding workloads. The timing places both US frontier labs' pricing in visible contrast with V4 Pro during the same enterprise purchase cycle, maximising the cost-comparison signal to procurement decision-makers.

NVIDIA occupies an unusual position on both sides of the ledger. Export controls limit GB300 access to Chinese labs, and V4's architectural efficiency is explicitly designed to operate within those constraints. The concurrency analysis from @bookwormengr (via @huggingface) demonstrates that V4's 10× throughput density improvement is hardware-agnostic: any inference operator on any compatible hardware benefits from the KV cache reduction. Jensen Huang's argument — that China will build its own chips regardless, so they should be built on US technology — applies symmetrically in reverse: US enterprises will adopt Chinese open-source models regardless, so the strategic question is which stack they build on.

Enterprise buyers are the swing constituency. The procurement calculus Berman describes is direct: a CEO deploying AI for business workloads — not frontier research — faces a binary choice between US frontier API pricing and V4 Pro's near-equivalent capability at a fraction of the cost, with the additional option of fine-tuning and self-hosting open weights. The strategic and information-security dimensions are real but secondary to operating budget authority in most enterprise environments.

Trajectory

The core technical contribution of V4 is the hybrid attention stack. Tim Carambat's analysis (YouTube) correctly frames V4 as "a vessel for a new attention mechanism" rather than primarily a frontier model advance. The distinction matters: CSA+HCA is an in-weights compression mechanism, not a post-hoc runtime optimisation like quantisation. The KV-cache savings cannot be engineered away by competing approaches — they are structural to any deployment of V4, including self-hosted inference once vLLM, SGLang, and llama.cpp add support for the new attention operations.

The two mechanisms interact layer-by-layer:

Compressed Sparse Attention (CSA) groups every 4 KV tokens into a single compressed entry, then applies top-K sparse selection across those compressed blocks. The result is compression plus sparsity — faster indexing and substantially reduced memory footprint for attention computation at each layer.

Heavy Compressed Attention (HCA) is more aggressive: every 128 KV tokens collapse to a single entry, with no sparsity layer applied. Attention runs directly over the compressed stream. According to the Developers Digest technical breakdown (YouTube), this is where the majority of the 90% KV reduction originates. Both mechanisms are interleaved layer-by-layer alongside a conventional sliding-window attention branch that preserves fine-grained local token detail — preventing aggressive compression from losing positional precision required for multi-step reasoning.

On aggregate throughput, the numbers are decisive. At 1 million tokens on a GB300 NVL72 (176 GB HBRAM), V3.2 consumed 35.60 GB of KV cache and supported 4 concurrent requests. V4 reduces that to approximately 3.56 GB, enabling roughly 40 concurrent sessions. For inference operators, this is a 10× improvement in throughput density at constant hardware cost — a change that directly reprices the economics of serving long-context agentic workloads at scale. The Developers Digest analysis notes that V4 is explicitly marketed for agent loops, referencing Claude Code and OpenCode-style harnesses by name, a positioning decision that targets the exact workload where the KV cache savings are most operationally valuable.

The benchmark profile is strong but uneven. V4 Pro Max-Thinking competes directly with Opus 4.7 and GPT-5.5 on most knowledge-intensive and agentic evaluations. However, two independent real-world tests reveal a strategic reasoning gap. Discover AI's causal-reasoning puzzle — a multi-constraint elevator optimisation problem — found V4 Pro Sinking crashing mid-solution and never recovering, while V4 Flash Sinking solved the same problem in 9 button presses. The exposed reasoning trace, which V4 releases without summarisation (making it unusually transparent for distillation analysis), shows a "do it, go there, see what happens" trial-and-error pattern rather than strategic decomposition. BridgeMind's proprietary BridgeBench independently placed V4 Pro dead last in its evaluation cohort. These findings are consistent with the pass@1 benchmark methodology DeepSeek used — noted by Carambat as atypical relative to the ML community's standard of pass@3 or pass@5.

The current local inference ecosystem gap is temporary. vLLM, SGLang, llama.cpp, Ollama, and LM Studio all require architecture updates to support CSA+HCA. The HuggingFace ecosystem, which tracked V4 to #1 trending on the platform in 43 minutes after release (source), will likely produce inference stack updates within weeks. When that happens, V4's efficiency gains become available for fully local deployment on approximately 128 GB of consumer GPU memory — a meaningful reduction from the 200+ GB previously required for 1M-context windows at comparable throughput.

Implications

Enterprise AI procurement is the near-term inflection point. US frontier API pricing at $25–30/M output tokens was defensible when the capability differential was large enough to justify the premium. V4 Pro Max-Thinking's near-parity on most business-relevant benchmarks, combined with open weights and fine-tuneability, brings the cost-benefit calculation to a threshold where rational enterprise procurement decisions increasingly include V4 as a cost-optimised alternative for workloads that do not require frontier-edge capability. The downstream effect on US lab revenue projections is not trivial: even a 10–15% shift of enterprise workloads to V4 represents meaningful revenue compression at the margin for labs whose capital structures assume expanding enterprise API revenue.

The US AI investment thesis faces a specific stress scenario. The US AI infrastructure buildout — characterised by Oracle's recently closed $16B Michigan data centre financing dedicated to OpenAI applications, and by trillions in projected capex — is predicated on US-trained, US-served frontier models capturing the global enterprise stack and generating returns proportional to that capture. V4-class open models at one-eighth the API price, with full fine-tuneability and self-hosting potential, shift enterprise adoption patterns away from US-served APIs. At scale, this compresses the addressable revenue for US frontier labs and raises questions about the return profile on AI infrastructure capex that is currently being committed.

Information control and cultural alignment carry longer-horizon risk that Berman articulates directly: enterprise software built on DeepSeek models encodes DeepSeek's content policies, refusal patterns, and behavioural alignment into the workflows of global businesses. The mechanism differs from social media — enterprise AI is B2B, not consumer-facing — but the governance principle holds. At scale, model behaviour becomes an invisible layer over business logic. Whether DeepSeek's current content policies represent a material compliance concern for Western enterprises is a function of specific deployment context; the point is that the evaluation needs to happen explicitly, not by default.

Export controls are producing the intended short-term effect — a computational ceiling — but not the intended long-term structural outcome. DeepSeek's algorithmic innovation has partially compensated for the hardware gap. The Huawei Ascend 950 confirmation accelerates the divergence: China is building a sovereign hardware stack specifically aligned to V4's architecture, which will erode the compute-constraint ceiling as the 950 supernodes scale in H2 2026. The US government's formal distillation-attack acknowledgment is a response to symptom rather than cause — the algorithmic capability being built on constrained hardware is the more durable dynamic.

For Anthropic specifically, the competitive geometry is challenging. A company characterised as "demand-rich, compute-starved" relative to OpenAI, Google, and xAI is simultaneously facing a near-parity open-weight alternative at one-eighth its API price. The quota-reduction mechanism described in the April 25 commentary increases user incentive to evaluate alternatives at the same moment V4 provides a credible one. If V4's strategic reasoning gaps — currently its most defensible quality differential — are addressed in subsequent releases or through fine-tuning, Anthropic's differentiation narrows to the frontier edge of the capability distribution: a market segment that is real but smaller than the full enterprise stack Anthropic's revenue model requires.

Outlook

Two events define the near-term timeline: the H2 2026 rollout of DeepSeek's 950 super nodes at scale, and the inference ecosystem updates that will unlock CSA+HCA architecture support in vLLM, llama.cpp, and compatible local stacks.

The supernode rollout will reduce V4 Pro API pricing materially — the white paper is explicit. A model already 7–9× cheaper than US frontier alternatives becoming 2–3× cheaper still would meaningfully accelerate enterprise adoption and reduce the cost threshold for self-hosted deployments. Whether this lands in Q3 or Q4 2026 depends on Huawei's Ascend 950 production ramp and DeepSeek's deployment execution.

The inference stack updates are a matter of weeks to months. Once they land, the full efficiency profile of V4 — including the 10× concurrency density gains — becomes available to any organisation capable of self-hosting on GPU memory in the 128 GB range. This extends the price advantage to organisations that can amortise hardware costs, driving the effective cost-per-query well below DeepSeek's own API pricing.

Berman's two strategic prescriptions for the US — more open-source frontier work and aggressive API cost reduction — are both constrained by the same factor: compute availability and structural incentives at the frontier labs. Google is the US lab closest to open-source frontier work via Gemma and related releases, but has not fielded open weights at V4's scale. OpenAI and Anthropic are not structurally oriented toward open-weight releases at frontier scale.

The monitoring variables for any organisation tracking this landscape: DeepSeek Pro pricing announcements post-supernode-scale in H2 2026; benchmark performance on strategic reasoning tasks where V4's trial-and-error pattern is currently its primary gap; US lab responses in pricing, open-source posture, or efficiency-oriented architectural research comparable to CSA+HCA; and the pace of Huawei Ascend 950 production ramp as the enabling hardware constraint. The next 90 days are likely to determine whether V4 represents a peak disruption moment or the opening phase of a sustained efficiency-parity era in open-weight AI that structurally alters the US frontier lab revenue model.